Knowledge Bank

Crypto Bullruns Past and Present

Apr 2024

By Kairon LabsKnowledge Bank

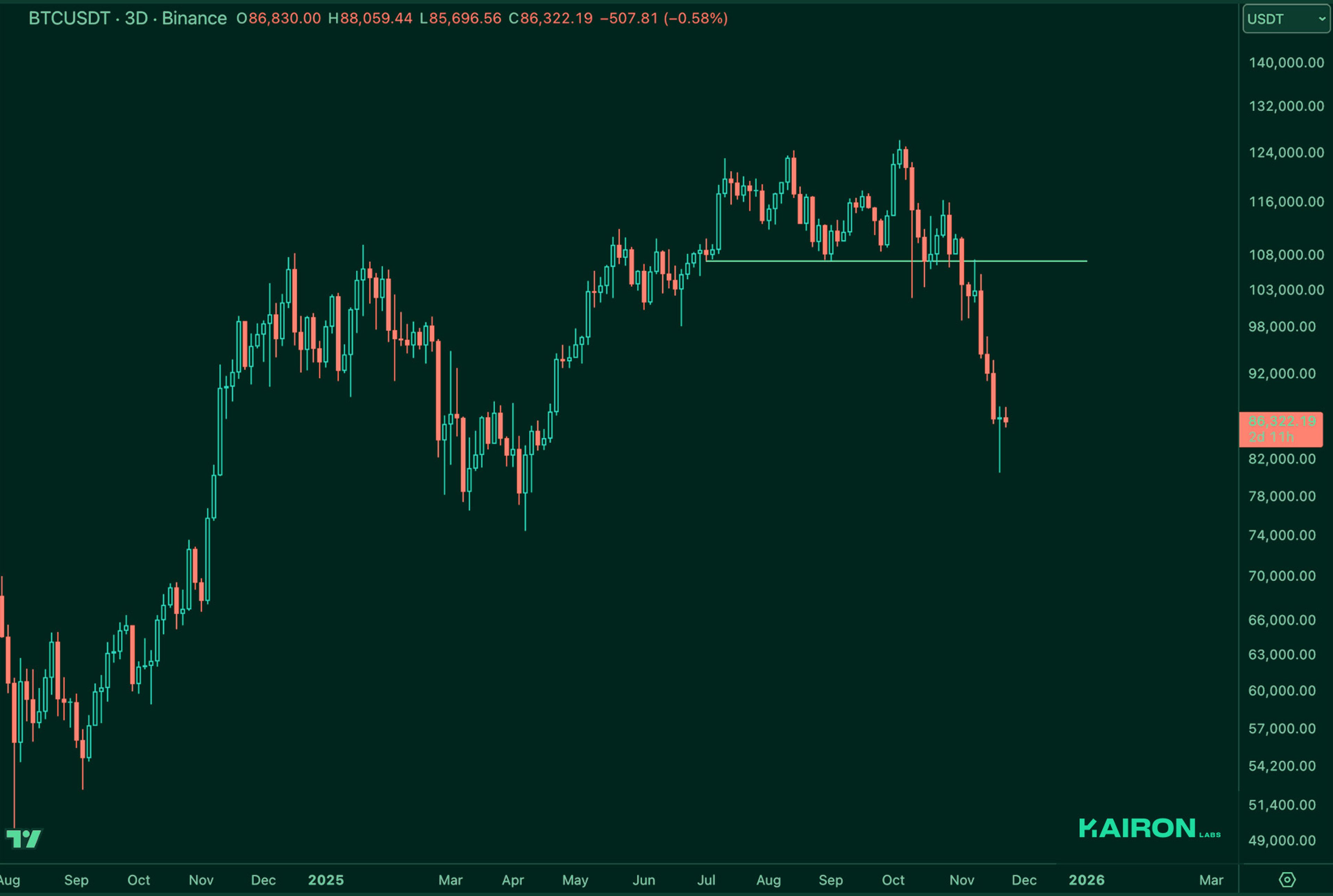

Markets remained volatile last week and traded within wide ranges with BTC hitting as low as ~$80k, levels seen in Q2 of this year, as markets took on a risk-off approach, as we thought and shared in our previous weekly update. This price action is despite the market initially reacting positively to NVDA’s strong earnings. The company exceeded expectations, which briefly boosted sentiment across risk assets on Wednesday after the US close. However, the bounce was short-lived in what was a classic “dead-cat bounce" move as traders returned their focus to the larger economic situation.

The turning point occurred when jobless claims data came in higher than expected, indicating a softer labor market. Rising initial jobless claims put more pressure on an already cautious market, suggesting that economic momentum may be slowing more quickly than anticipated. Meanwhile, the Manufacturing PMI remained above the key 50-point mark but still fell short of expectations. The message was clear: the economy is still growing, but not at the pace that markets had hoped for.

Regarding crypto, BTC Spot ETF flows last week signaled that sentiment was indeed defensive. The week began with consistent selling pressure, as November 17 and 18 experienced back-to-back outflows of -$254M and -$372M. Mid-week, the mood improved briefly. On November 19, there was a small inflow of $75M, the first sign that some buyers were ready to return as the market digested NVDA’s impressive earnings report.

That optimism didn’t last long though. On November 20, there was a massive outflow of close to 1 billion at -$903M, the largest of the week. This clearly indicated that institutional investors may have been reducing their exposure aggressively. Only on Friday did flows stabilize again. November 21 ended the week positively, with +$238M in inflows, suggesting that bargain hunters or rebalancers entered the market after the heavy mid-week decline. Despite the bounce at the end of the week, the overall trend remained clearly cautious. Total net assets dropped sharply from $121B at the beginning of the week to $110B by Friday. This highlights the significant impact of ongoing outflows on ETF holdings during the macro-driven pullback.

This week brings several important data releases that could change market views as the year ends. PPI will provide insights into inflation trends on the producer side, while the upcoming GDP report will help determine if the slowdown mentioned in recent surveys is happening. Initial jobless claims will also again be closely monitored following last week’s disappointing data. Together, these metrics should offer a clearer picture of the economy’s health, inflation trends, and the strength of the labor market. We will also receive retail sales and consumer confidence numbers, two key indicators as we head into the holiday season. With consumer spending making up a significant portion of U.S. economic activity, these reports will indicate whether households are ready to support growth or if caution will hinder Q4 momentum.

Overall, the market remains sensitive to each data point. With sentiment fragile after last week’s quick decline in risk appetite, traders are preparing for another week where economic data releases could lead to significant changes in positioning. However, with most of the macro fundamentals seeming to be priced in for 2025, we should see some relief going into the rest of Q4 if we don’t have any other macroeconomic surprises. We remain cautious but will monitor price action carefully to capitalize on any 'relief rally' or spikes into year-end.

The magnitude and depth of BTC’s decline have materially exceeded our initial expectations. The market continued to unwind leverage until it finally tapped the February 2025 high-volume node, which is where we saw the first meaningful rebound. On the daily timeframe, BTC is now deeply oversold, and short-term momentum indicators are showing clear signs of exhaustion. That said, the broader structure has not completed a full reversal, and a secondary retest of the lows remains a realistic scenario. We will be watching the efficiency of any pullback from here and whether BTC can establish a higher structural low to confirm that a durable bottom is forming.

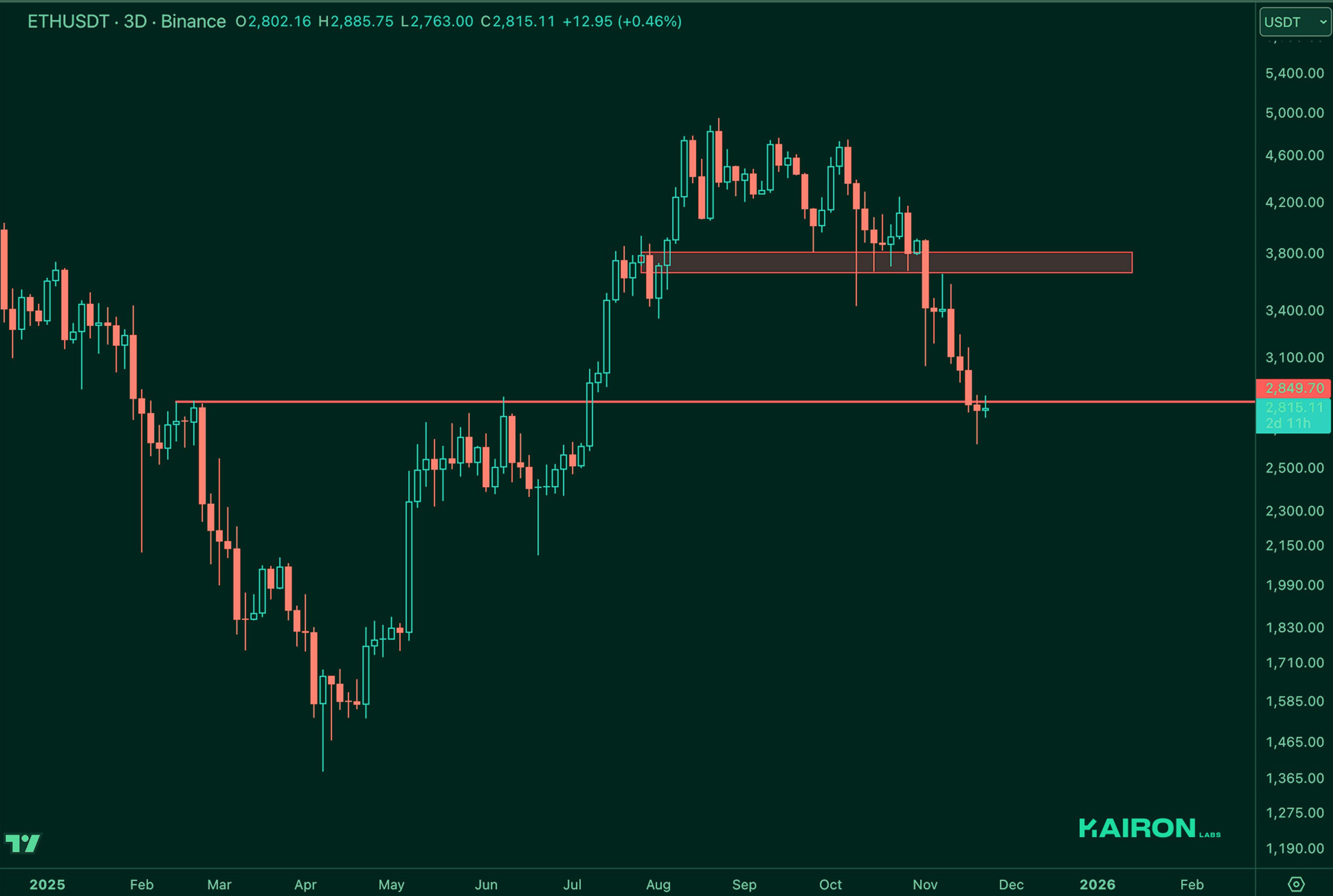

ETH failed to show any meaningful absorption at the expected support zones. Instead of stabilizing at the initial key levels, the market sliced through them with little resistance and only found buyers much deeper in the structure. The rebound we are seeing now is occurring well below the prior breakdown area, which underscores how one-sided the liquidation flow was during the selloff.

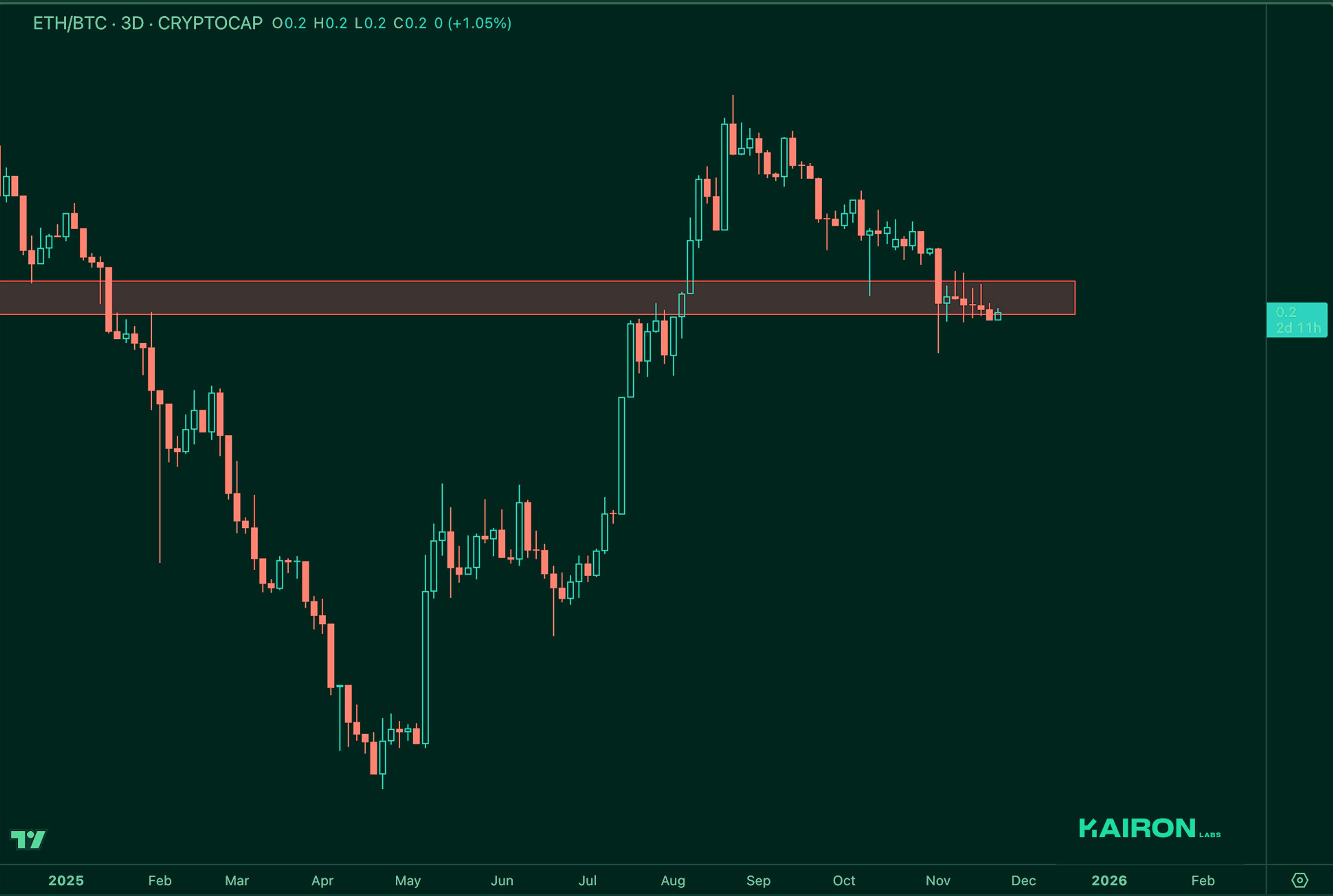

ETH/BTC remains stuck in a tight, stagnant equilibrium. The pair is sitting inside the prior breakdown zone with neither side able to establish directional conviction. Despite the broader volatility across majors, ETH/BTC has shown almost no follow-through, reflecting a clear stalemate in relative strength.

TOTAL3 continues to trend lower in an uninterrupted, one-way fashion. Until we see a decisive shift in momentum or a reclaim of any of the major breakdown levels, the path of least resistance remains to the downside. The market is effectively pricing in continued deleveraging across the altcoin complex, and any sustainable inflection will likely require a reset of positioning as well as stabilization in BTC and ETH first. For now, TOTAL3 remains in a controlled downtrend with no structural bottom in place.

Even with TOTAL3 firmly trending lower on an absolute basis, the TOTAL3 versus BTC cross continues to trend higher. This tells us that the relative bid into alts is outperforming BTC at the margin, despite the broader weakness across the complex. In other words, alts may be weak, but BTC has been even weaker on this leg.

This is the first time since 2024 that the Market Leverage Ratio has broken below its long-standing structural support. Although the indicator briefly dipped under the range and quickly reclaimed it, the message is clear: the market is probing the lower bound of a level that has defined every major cyclical bottom over the past two years. Unless we see a strong and convincing reversal from this zone, the risk profile becomes materially more fragile. A failure to hold here would imply that the deleveraging phase is not finished and that positioning could unwind further, potentially triggering a broader risk-off extension across the asset class. For now, the reclaim keeps the door open for stabilization, but the burden of proof sits firmly on the bulls.

DISCLAIMER:

The information in this report is for information purposes only and is not to be construed as investment or financial advice. All information contained herein is not a solicitation or recommendation to buy or sell digital assets or other financial products.

This post was prepared by the Kairon Labs Trading Team.

Edited for publication by: Shirley Castro

Kairon Labs provides upscale market-making services for digital asset issuers and token projects, leveraging cutting-edge algorithmic trading software that is integrated into over 100+ exchanges with 24/7 global market coverage. Get a free first consult with us now at kaironlabs.com/contact