Knowledge Bank

Crypto Bullruns Past and Present

Apr 2024

By Kairon LabsKnowledge Bank

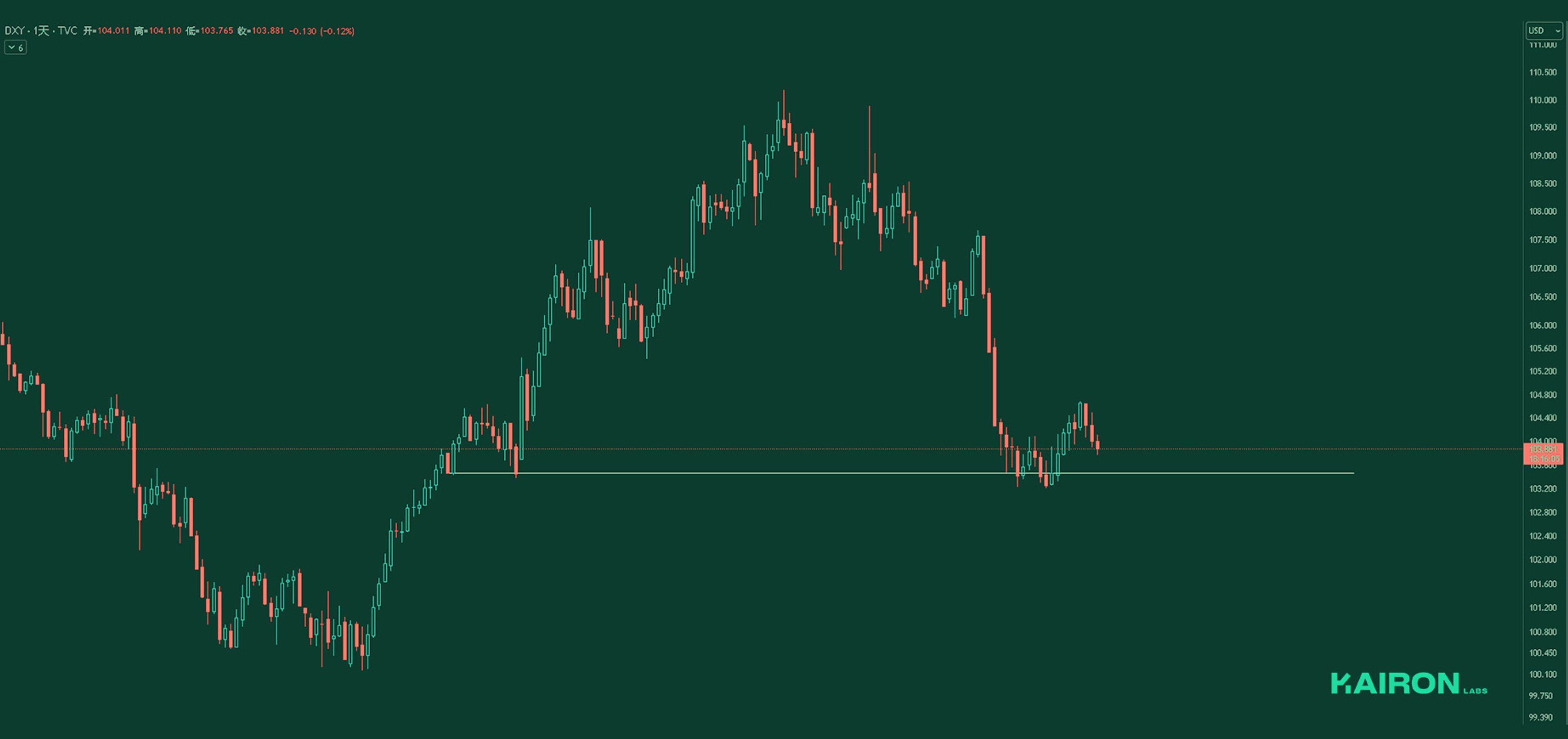

DXY continues to trade within the 103-105 range. The short-lived rebound has faded, and the index may need more time to consolidate sideways before the next market-moving catalyst emerges.

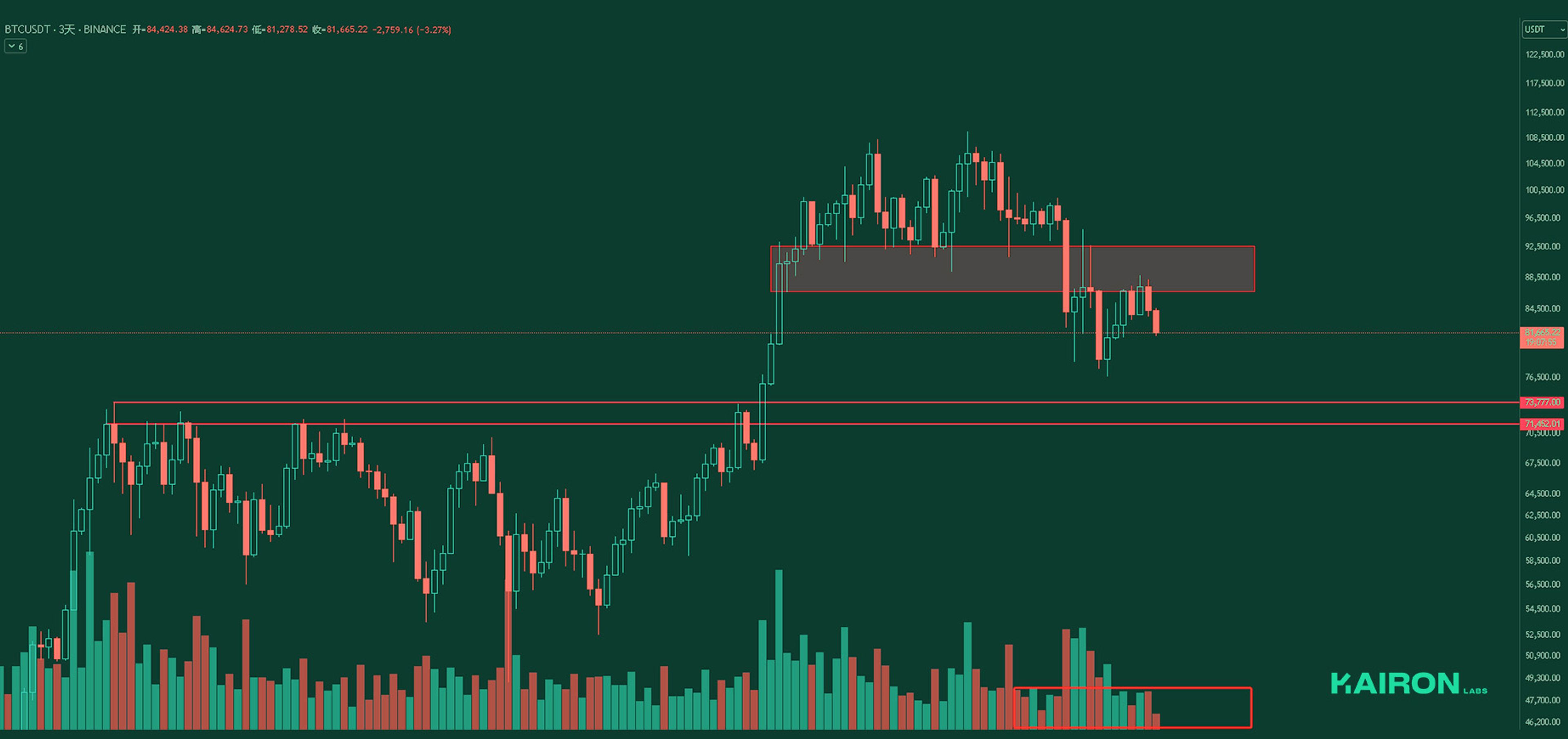

BTC's weak low-volume bounce stalled at the key supply zone before reversing—validating our earlier skepticism about the rally's sustainability. The rejection signals another failed upside attempt, increasing the risk of a deeper pullback.

ETH’s daily bullish structure was invalidated after Friday’s breakdown, leading to a swift retest of prior swing lows. A failure to establish a double bottom here may open the door for further downside, with the next key support level coming into play.

ETH/BTC keeps breaking to fresh record lows, and while the RSI is now in extreme oversold territory, ETH momentum remains absent.

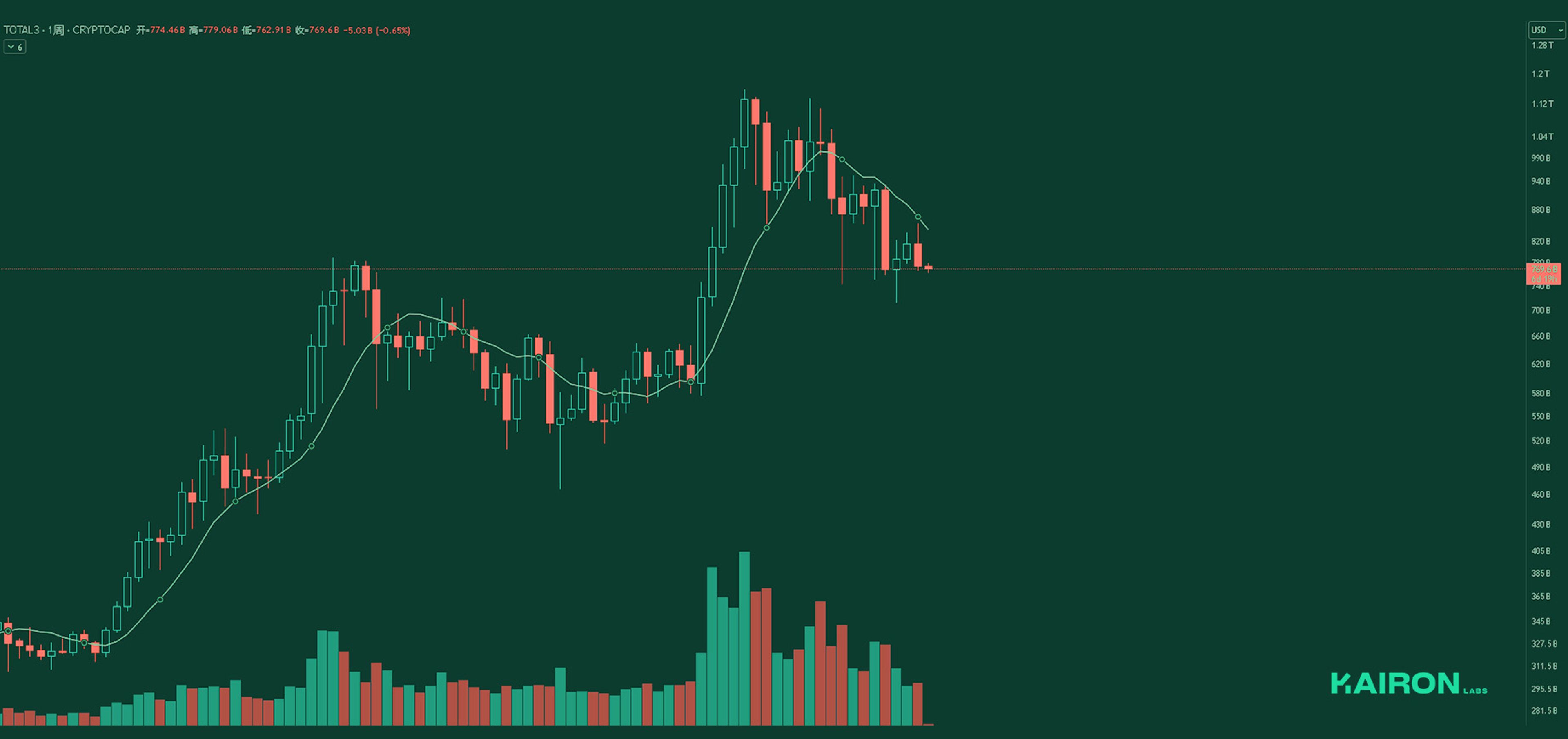

Total3 has completely surrendered its gains from the prior bounce, forming a weekly bearish reversal candle below the MA10. The breakdown indicates weakening momentum, increasing the odds of a retest of deeper support level ahead.

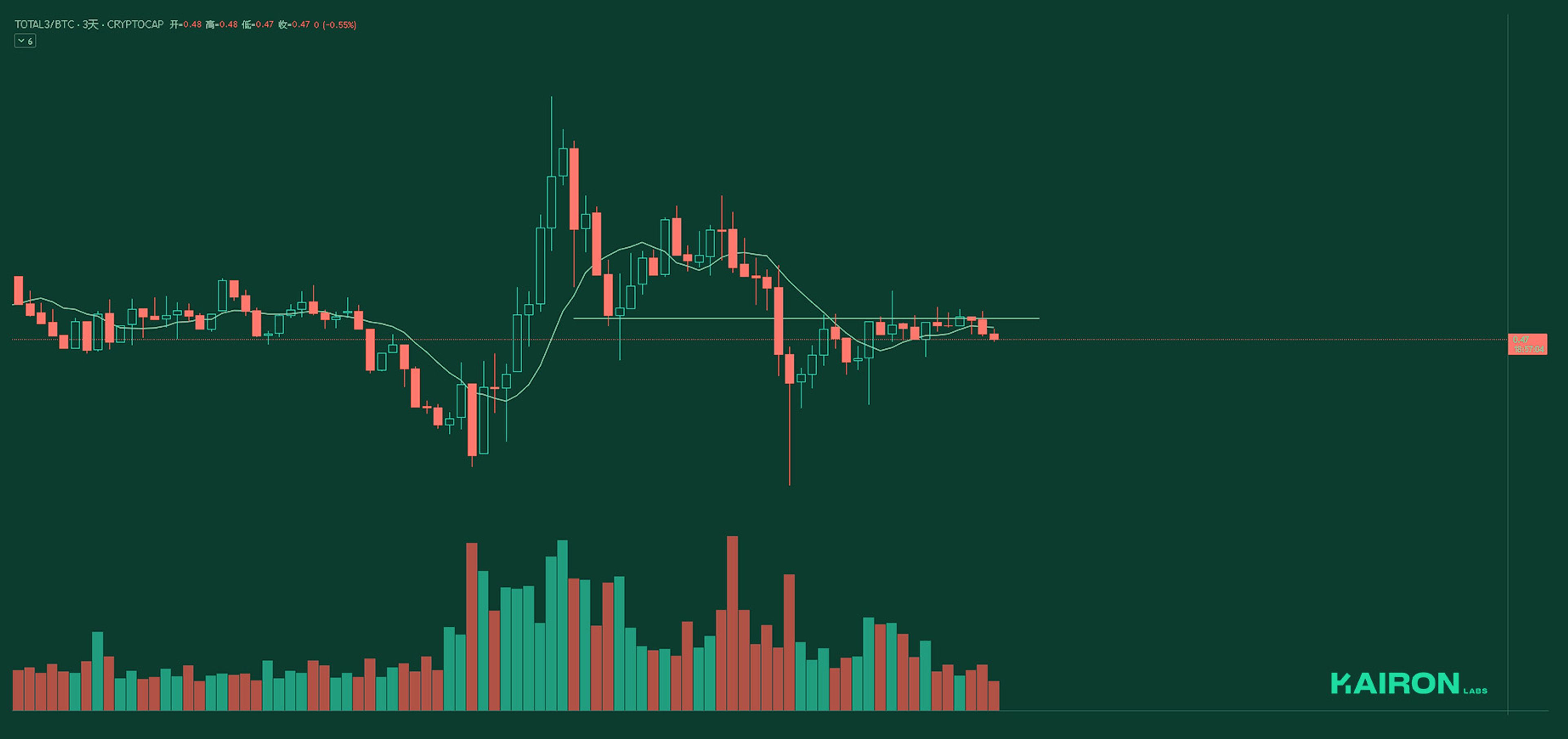

Total3/BTC faced rejection once again, unable to sustain upward momentum or overcome critical resistance. This repeated failure highlights its underperformance compared to BTC, keeping the bearish structure intact unless a decisive breakout occurs.

As the market continues to weaken, the Market Leverage Ratio has dropped further, signaling deteriorating risk appetite and declining trading activity.

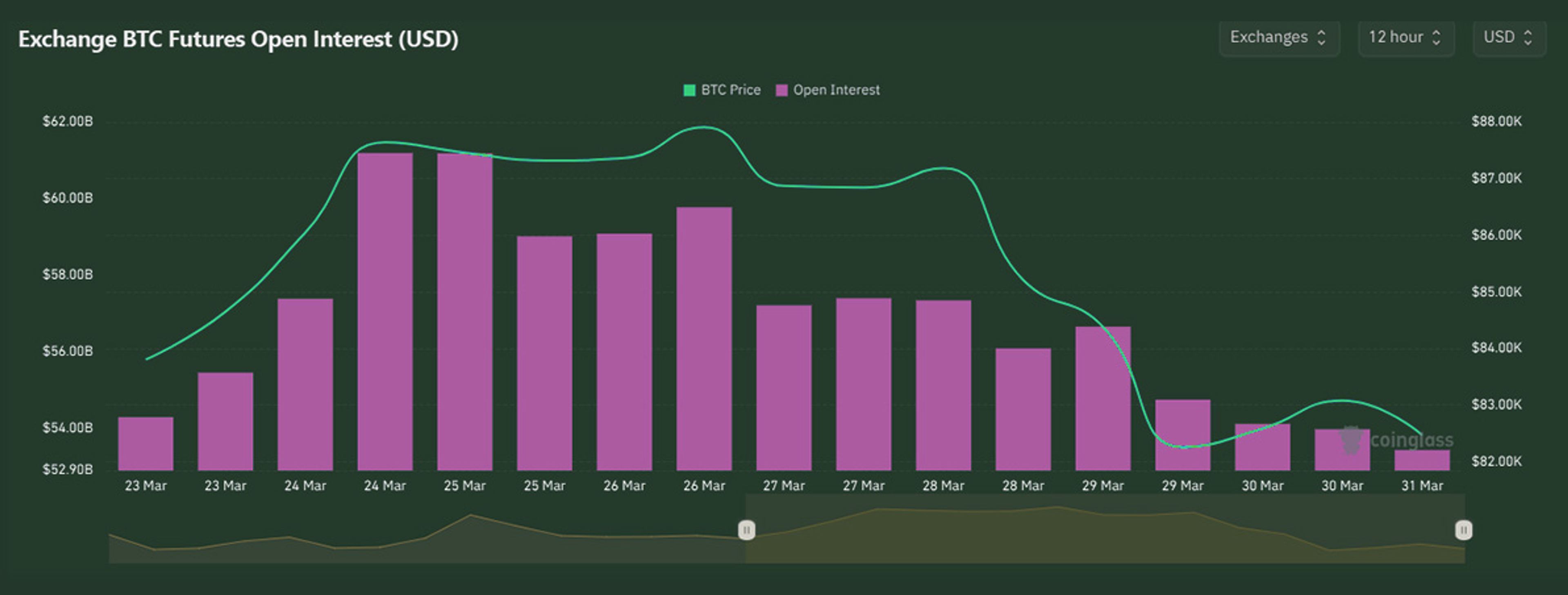

While OI has been on the decline since Bitcoin’s ATH, indicating an overall decrease in speculative and hedging activity, we are seeing an increase in OI in March along with the rebound in BTC, indicating a possible continued momentum increase in the price action.

Similarly, OI decreased together with the decrease in ETH price.

However, while we see a reduction in OI, the reduction is not as significant as that in BTC, which can indicate that there could be continued downward momentum to come

BTC perps funding went negative early in the week when it reached the week highs of 88k, indicating shorts piling in. However, as the coin started to reverse and sell off, funding increased significantly, as more speculators tried to long the dip.

Funding eventually ended slightly negative, as bulls appeared to be outweighed by the bears towards the end of the week.

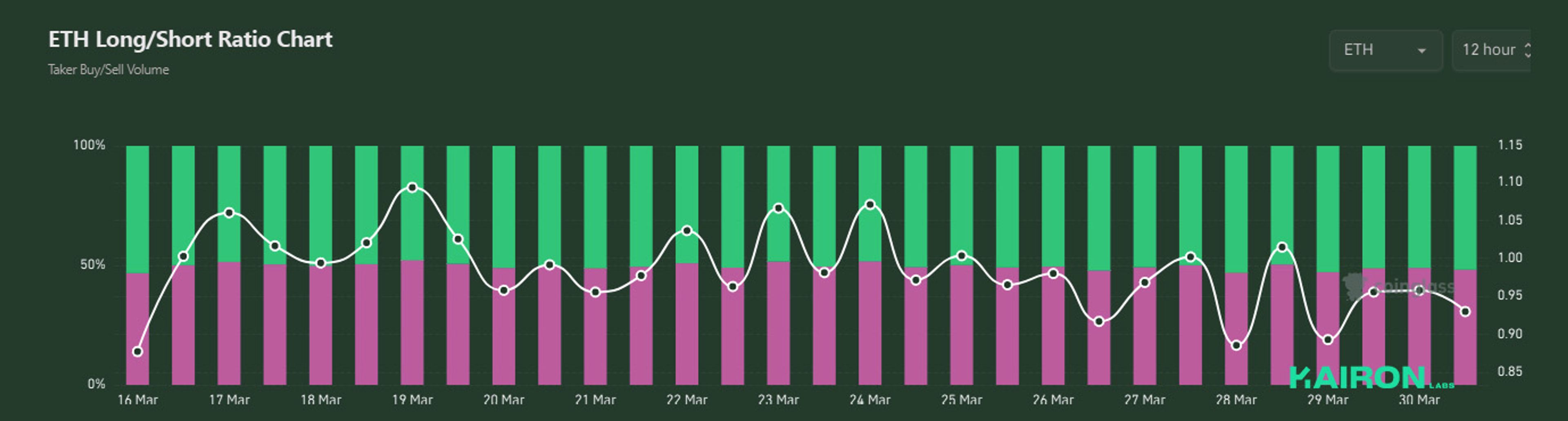

ETH funding remained positive for most of the week and throughout the selloff- showing market being biased long.

Funding did reach negative towards the bottom of the price range at the weekend, indicating bulls finally tapping out.

However, the persistence of funding remaining in positive showed that the market remained persistently long - which telegraphed the additional downside to come.

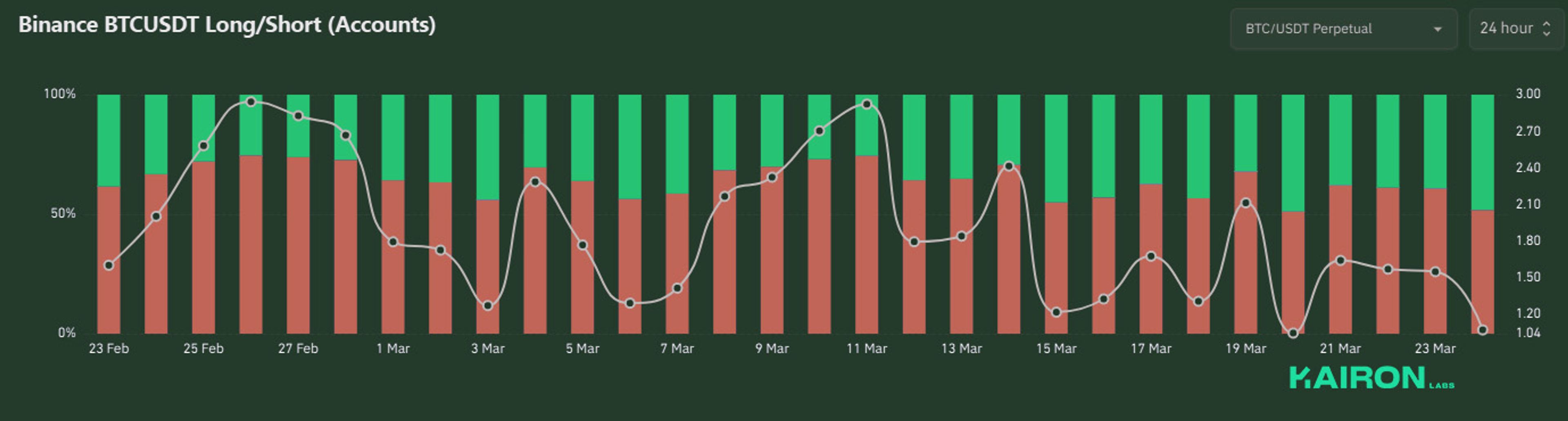

As indicated by the funding rate, the market remained slightly long to long at the start of the week, before shorts took over with long/short ratio flipping short towards the end of the week as prices declined.

The market was for the most part on the long side as indicated by the long/short ratio- which as mentioned, telegraphed the larger declines in price that would happen for ETH if declines happened.

The market eventually flipped short with the long/short ratio on the negative side as the price continued declining into the weekend.

DISCLAIMER:

The information in this report is for information purposes only and is not to be construed as investment or financial advice. All information contained herein is not a solicitation or recommendation to buy or sell digital assets or other financial products.

This post was prepared by Kairon Labs Trader Patrick Li, Travis Su, and Kenny Lee.

Edited by: Marianne Dasal

Kairon Labs provides upscale market-making services for digital asset issuers and token projects, leveraging cutting-edge algorithmic trading software that is integrated into over 100+ exchanges with 24/7 global market coverage. Get a free first consult with us now at kaironlabs.com/contact